Owning your home free and clear sounds amazing, right? No mortgage. No monthly payment. No lender lurking in your inbox like a caffeinated hall monitor. But here’s the not-so-fun plot twist: a paid-off home can be a juicy target for deed theft, title fraud, and other property scams.

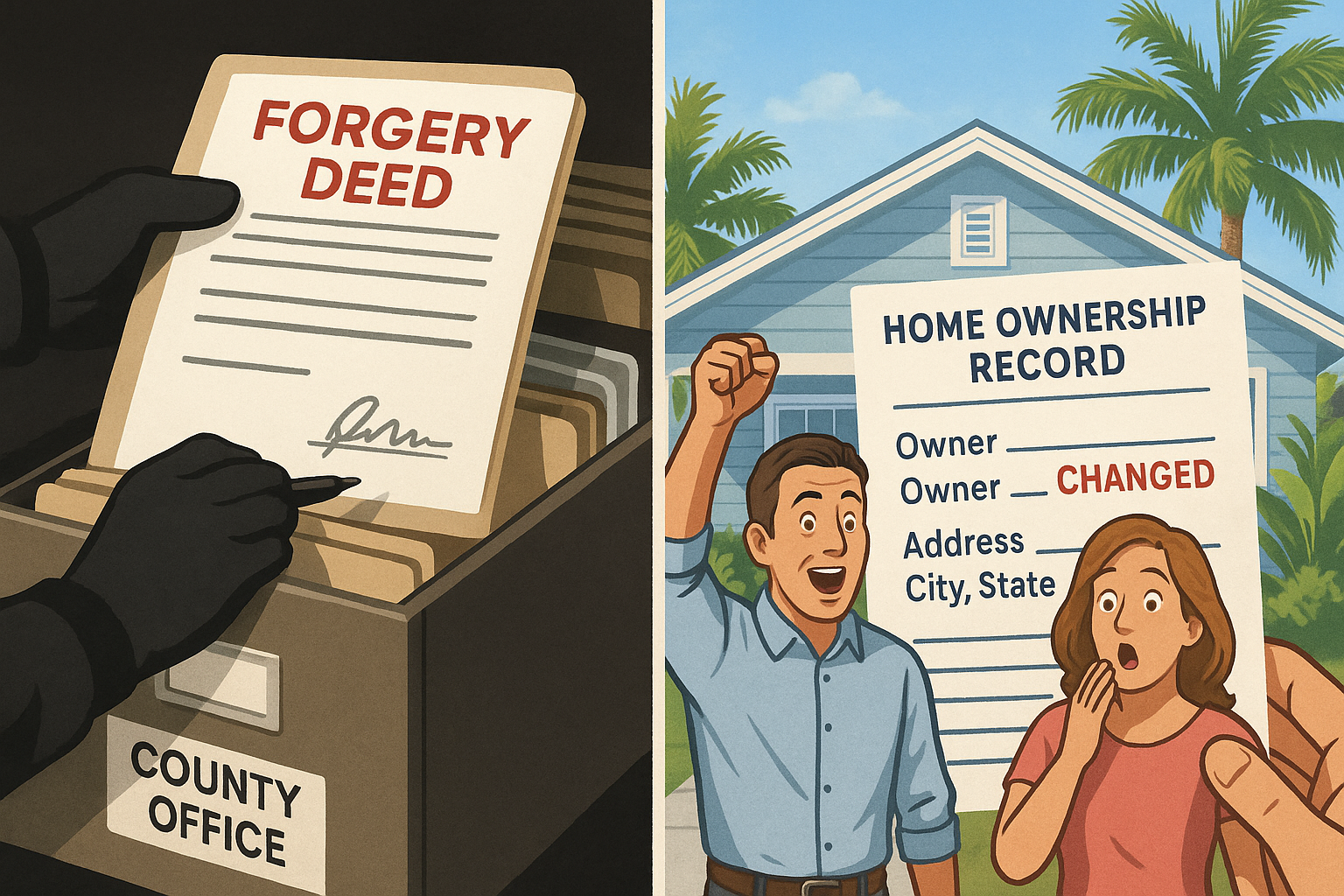

Here’s the quick definition: deed theft happens when someone illegally files paperwork to try to transfer ownership of your home without your permission. Title fraud is the broader mess that follows when a scammer tampers with ownership records, credit, or liens. In Florida, especially in busy markets like Tampa, keeping an eye on county records is smart real estate survival, not paranoia.

Let’s be real—when there’s no lender watching the title, a scam can sit quietly in the background like a raccoon in the attic. And by the time you notice, the damage may already be in motion.

The good news? There are practical ways to protect yourself. Some are free. Some are low-cost. And a few can save you from a paperwork nightmare that makes tax season look like a beach vacation.

What Is Deed Theft or Title Fraud?

Deed theft, title fraud, and property fraud all boil down to the same ugly idea: someone illegally tries to transfer ownership of your property without your permission.

In many cases, it starts with identity theft. A criminal pretends to be the homeowner and files fake paperwork to move the deed. Once they’ve done that, they may try to:

– Sell the property

– Take out a loan against it

– Rent it out

– Use it as collateral

– Create legal confusion that freezes your ability to sell or refinance

Now, before your eyes glaze over like a fresh donut, here’s the important part: paid-off homes are often targeted because there’s no mortgage company keeping tabs on the title. That doesn’t mean mortgaged homes are immune. It just means free-and-clear homes can take longer to detect fraud.

Takeaway: If someone can fake ownership on paper, they can create a mess fast—so the goal is to catch weird activity early.

Why Paid-Off Homes Can Be More Vulnerable

A home with a mortgage usually has a lender receiving notices and watching for title problems. A paid-off home? Often fewer eyes, fewer alerts, and fewer chances to notice something shady.

That can make fraud easier to hide. A homeowner may not realize anything is wrong until:

– Tax bills stop arriving

– A loan notice shows up for a debt they never opened

– An unfamiliar deed appears in county records

– They try to sell or refinance and hit a title issue

– A stranger shows up claiming to be a tenant or buyer

Hot take incoming: fraud doesn’t always look like a dramatic movie break-in. Sometimes it looks like a boring document filed at the county office, which is somehow even more annoying.

Pro tip: If the scam leaves a paper trail, your best defense is checking the paper trail before it becomes a problem.

Common Signs of Home Title Fraud

If fraud is happening, it often whispers before it screams. Watch for these warning signs:

– Mail suddenly stops or gets redirected

– Property tax notices go to a different address

– Bills arrive that you don’t recognize

– A new deed or lien appears in public records

– Your credit report shows changes you didn’t make

– A notice arrives about a loan secured by your house

– Buyers, agents, or tenants contact you out of nowhere

The faster you spot suspicious activity, the easier it is to untangle. Think of it like a leaky faucet: annoying at first, catastrophic later.

Takeaway: If anything about your property mail, tax notices, or credit activity changes unexpectedly, investigate immediately.

The Best Ways to Protect a Paid-Off Home

Check Your Property Records Regularly

One of the simplest defenses is reviewing your county property records from time to time.

Look for:

– New deeds

– New liens

– Unauthorized mortgage filings

– Ownership changes

– Mailing address changes

Many counties now offer fraud alerts or property monitoring systems for free. These can notify you when a document is filed in your name or against your property.

If your county has a property fraud alert program, sign up. Yesterday would’ve been ideal, but today still counts.

Pro tip: Set a calendar reminder to check your property records a few times a year. Future-you will be very grateful and slightly smug.

Monitor Your Mail and Tax Statements

The FTC and title experts consistently recommend keeping a close eye on your bills and tax notices.

Be suspicious if:

– A property tax bill is late or missing

– You stop receiving utility or tax mail

– A notice arrives with unfamiliar account details

– You get mail about a transfer you didn’t authorize

Scammers may try to intercept mail or redirect it so you don’t catch the fraud quickly.

Takeaway: Mail may seem old-school, but in title fraud cases, it can be your first warning sign.

Review Your Credit Reports

Sometimes fraudsters use stolen identity details to open loans or connect debt to a property.

Check your credit reports regularly for:

– New accounts you don’t recognize

– Inquiries from unfamiliar lenders

– Address changes

– Mortgage-related activity you didn’t authorize

You can get free credit reports through AnnualCreditReport.com. If anything looks off, dispute it right away.

Pro tip: A credit report is like your financial security camera footage—boring, but incredibly useful when something weird happens.

Sign Up for County Fraud Alerts

Many counties and recorder’s offices now offer free fraud notification systems.

These alerts won’t stop every scam from happening, but they can warn you quickly if a document is filed under your name or property address.

That matters because time is everything. The sooner you catch a fake deed, the better your odds of stopping further damage.

Takeaway: County alerts are one of the easiest, lowest-cost layers of protection you can use.

Keep Personal Information Tight

A lot of title fraud starts with identity theft. That means protecting your personal info is not optional—it’s the whole game.

Do this:

– Shred documents with personal data

– Avoid oversharing ownership details online

– Secure old closing documents

– Use strong passwords and multifactor authentication

– Watch for phishing emails and scam calls

Fraudsters often only need enough information to fake signatures, notarizations, or identity documents.

Pro tip: If your social media says you’re “traveling for three weeks” and your mailbox is overflowing, that’s basically an engraved invitation for trouble. Don’t do the scammer’s marketing for them.

Consider Owner’s Title Insurance

This is one of the most important protections for a paid-off home.

Owner’s title insurance is different from “title lock” marketing services. It’s a real insurance policy that may help protect you against covered title defects, including some fraud-related claims.

The FTC has warned that title lock services do not stop fraud. They may only monitor for changes after the fact. That’s not the same thing as insurance.

If you already have owner’s title insurance, review what it covers. If you don’t, ask a title professional or real estate attorney whether it makes sense for your situation.

Takeaway: Insurance protects; monitoring only reports. Those are not the same thing, even if the sales pitch says otherwise.

Be Careful With Paid “Title Lock” Services

The FTC has specifically warned consumers that “home title lock” is not a lock and not insurance.

These services often market themselves like they’re a safety net, but many simply monitor public records and send alerts after something has already been filed. Helpful? Sometimes. Enough? Not usually.

Before you pay, ask:

– Does it prevent fraud or only alert me?

– Does it offer legal help?

– Is it duplicating a free county service?

– Is it actually insurance or just monitoring?

If the answer is mostly “monitoring,” you may be paying for a fancy alarm clock after the house is already smoking.

Pro tip: Don’t confuse a notification service with real protection. That’s like buying a smoke detector and expecting it to put out the fire too.

Secure the Original Deed and Important Documents

Keep your original closing documents, deed, and title paperwork in a secure place.

Good options include:

– A fireproof home safe

– A bank safe deposit box

– Secure document storage with backups

If possible, keep encrypted digital copies too. Those records can help if you need to challenge a fake deed later.

Takeaway: Your documents are your evidence. Treat them like the keys to the castle, because legally, that’s kind of what they are.

What to Do If You Think Fraud Has Happened

If you suspect someone has tried to steal your home or file a false deed, don’t wait around hoping it disappears like bad carpet in a listing photo.

Take These Steps Immediately

1. Contact your county recorder or register of deeds

– Request copies of the suspicious filings.

– Report that you did not authorize them.

2. File a police report

– Get a report number and keep a copy.

3. Report identity theft

– Use IdentityTheft.gov to create a recovery plan and file an FTC report.

4. Notify your title insurance company

– If you have owner’s title insurance, ask what coverage applies.

5. Contact a real estate attorney

– You may need a quiet title action or other legal steps to restore ownership.

6. Alert credit bureaus

– Place fraud alerts or credit freezes if your identity was compromised.

7. Monitor taxes, mail, and county filings closely

– Keep watching for anything else connected to the property.

Fraud cases often require cleanup work, and cleanup work is much easier when you start fast.

Pro tip: Save copies of everything—emails, notices, filings, and phone logs. In fraud cases, the paper trail is your best friend.

Real-World Prevention Strategy for Homeowners

Here’s the simple, common-sense plan most paid-off homeowners can follow:

– Sign up for county property fraud alerts

– Check property records a few times a year

– Review your credit reports regularly

– Keep your deed and closing documents secure

– Watch your mail and tax bills

– Ask about owner’s title insurance

– Ignore or scrutinize “title lock” sales pitches

– Teach family members how to spot suspicious calls or mail

Do just these basics, and you’ll be ahead of a lot of homeowners who are assuming “paid off” equals “bulletproof.”

Takeaway: A little prevention beats a giant legal headache every single time.

Final Thoughts

A paid-off home is a major asset, and that makes it a target for fraudsters looking to exploit weak monitoring and stolen identity information. The best defense is layered:

– Watch your property records

– Protect your personal information

– Use county alert systems

– Understand the limits of title lock services

– Consider owner’s title insurance

– Act quickly if anything suspicious appears

The big takeaway? Don’t assume full ownership means full safety. A little prevention now can protect your home, your equity, and your peace of mind later.

If you’d like help thinking through your real estate risk, click this link to schedule a 15 minute call:

Contact me with any questions at [email protected] or reply to this post to subscribe to my monthly commercial real estate newsletter for more insights.